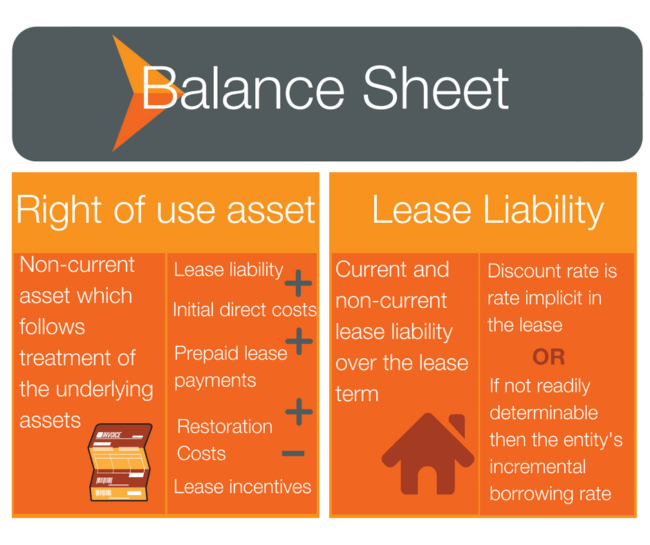

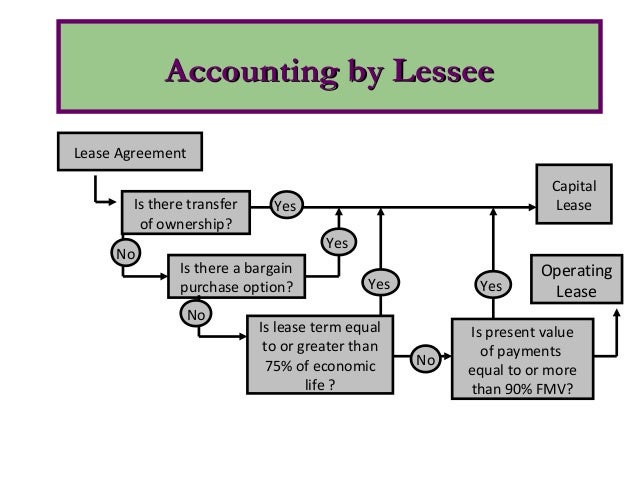

Capital Lease Accounting Example Lessee. Leases result in recognition of both an asset (often referred to as a right of use asset) and a lease liability in the books of the lessee at the commencement date. Now, let's look at the accounting treatment for a capital lease.

Capital lease accounting deals with the treatment of an asset rented by a business under the terms of a capital lease agreement.

The lease liability will be calculated as the present value (PV) of the future lease payments discounted using an appropriate rate.

New leases accounting standard AASB 16

The Best of IFRSbox 2016 - IFRSbox - Making IFRS Easy

What You Need to Know: Leases

How to Account for a Lease: 9 Steps (with Pictures) - wikiHow

Lease accounting

Capital Lease Accounting Under Current Accounting Standards

Personal Property Tax On Leased Vehicles - Property Walls

Capital lease accounting lessor example

Accounting for Leases under the New Standard, Part 2 - The ...

Capital leases are a bit more complicated. The new guidance requires lessees to recognize substantially all leases on their balance sheets as lease Example - Short-Term Lease Exception Permitted ABC enters into a contract to lease a piece of construction equipment Today's capital leases will be classified as finance leases, and today's. Delta transactions if treated as a capital lease.